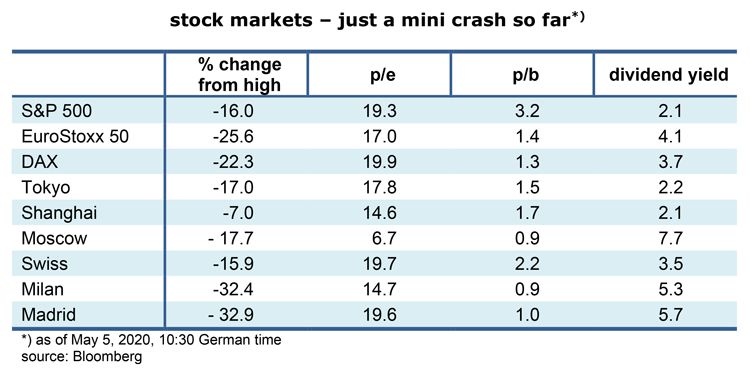

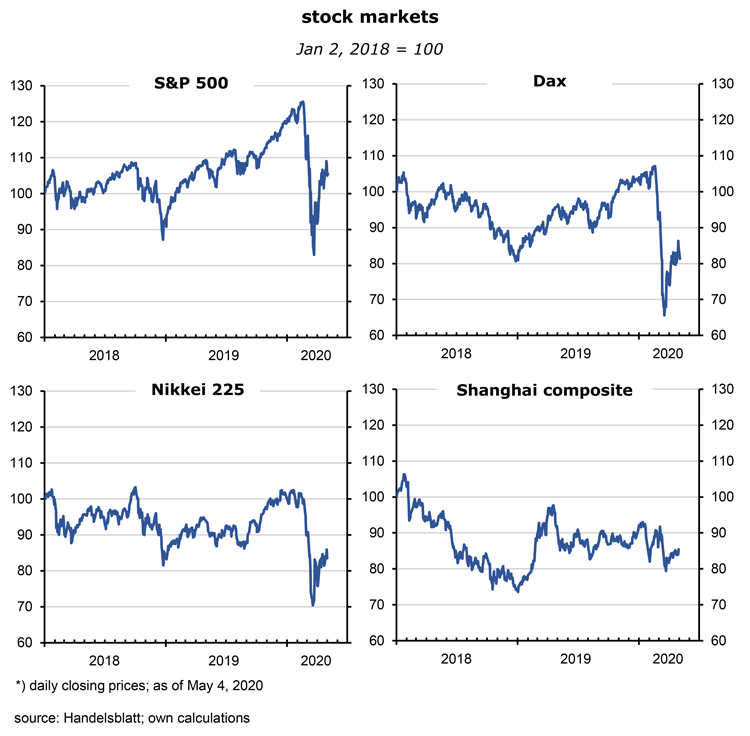

Stock markets ignore Corona – so far

- It is hard to believe that global stock markets have largely shrugged off the prospect that the world economy is approaching a full-scale depression, characterized by plummeting profits, widespread corporate defaults and record high unemployment. As the following table shows, the market correction has mostly been modest and not larger than what one would expect after a strong rally – nothing special. Most investors seem to suffer from a bout of wishful thinking.

China’s and America’s stock markets almost unaffected by economic slump

- Shanghai in particular has been down from its all-time high by just 7%, a number which is close to the typical weekly volatility. China seems to be, or wants to be, back to normal. It has been at the origin of the pandemic and got out of it earlier than other countries. But the CSI 300 does not reflect the hit real GDP is about to take.

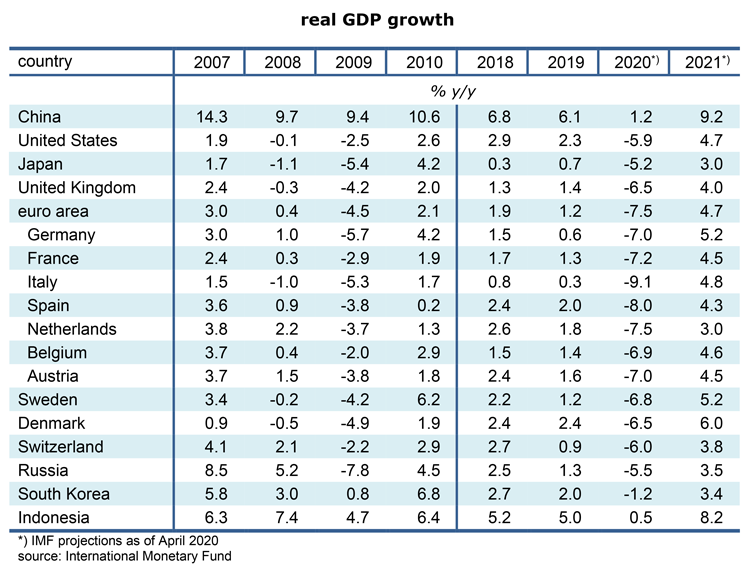

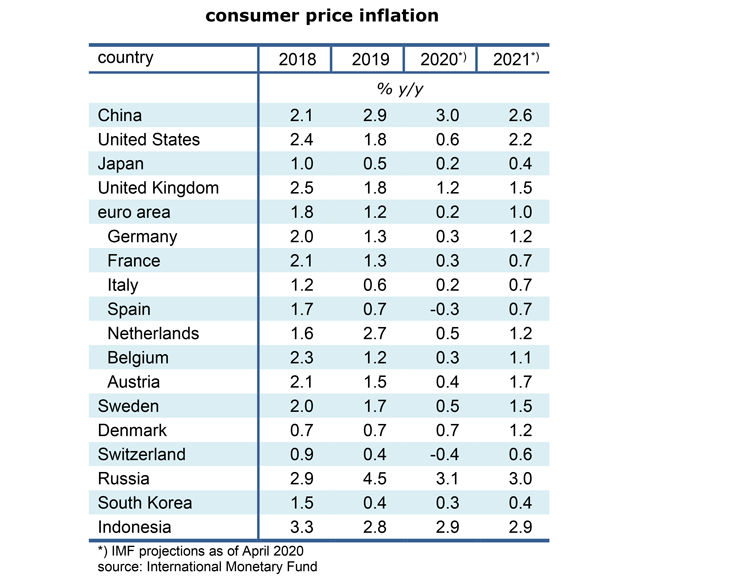

- As the next table shows, the IMF predicts that China’s growth will be just 1.2% y/y in 2020 which is far below recent trend growth rates of 6 to 7%. It means that there is a huge and rising output gap. Idle capacities exist in most export industries, in airlines, shipping and in many other sectors. Firms are struggling to generate profits and cashflow. Without a quick economic recovery in other countries – which is not yet on the horizon -, Chinese exports will be a drag on overall demand. Stock markets have only one way to go in the medium term: down.

- American stock markets are also surprisingly resilient. At one point this year, gripped by the Corona scare, they had declined, ie, crashed by 34% from February’s all-time peak, but then rebounded quite vigorously and are now just 16% below. Investors are convinced that the massive fiscal stimulus of the Trump administration will do the trick and prevent the US economy from sliding into a recession.

- This week’s American statistics will be terrible. Based on the number of initial jobless claims, it is now likely that the key employment number, nonfarm payrolls, will decline by about 21 million between March and April, from 151 million to 130 million, and send the unemployment rate up from 4.4% to 16% (on May 8). Auto sales have fallen by more than half from last year, and airline traffic has almost come to a standstill. Real GDP had declined at an annualized rate of 4.8% q/q in the first quarter of this year, but market analysts expect there is worse to come in Q2 – a seasonally adjusted annualized rate of an unprecedented -35%. These are depression era numbers.

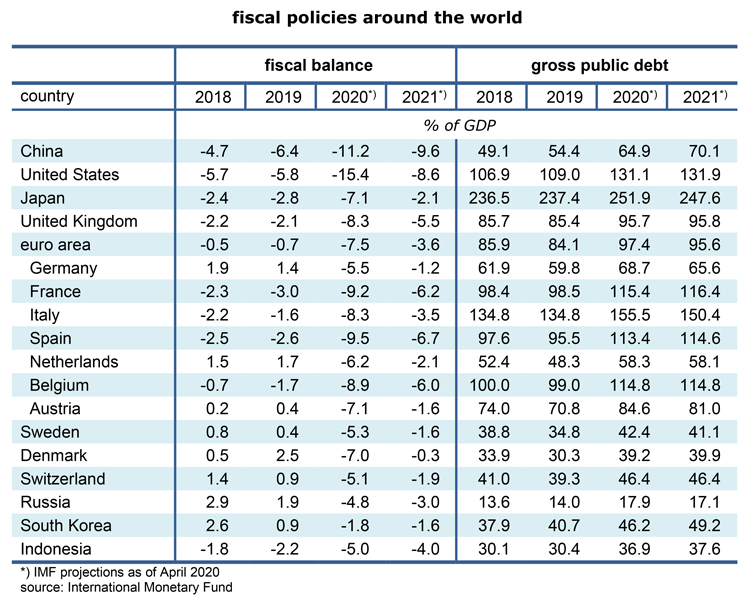

- That the projected budget deficit of 15.4% of GDP has been welcomed by stock markets looks plausible – firms like any increase in demand for their goods and services -, but that it has neither weakened the market for US Treasuries nor the dollar is something one has to get used to. Nor have longer-term inflation expectations been affected; according to inflation-protected government bonds market participants expect an average inflation rate of just 0.68% over the next five years. Consumer price inflation is presently around 1½ %.

- Dollar assets are attractive these days – the price-to-book ratio is no less than 3.2. Together with Swiss stocks and bonds they are regarded as the ultimate safe haven. Investors believe that the close cooperation of American fiscal and monetary policies will quickly lift the economy out of the doldrums. Both the administration and the Fed have the will as well as the necessary tools to succeed, and budget deficits can always be covered by money printing, by buying unlimited amounts of newly issued government and corporate bonds.

- This is something neither the Italian or Spanish, nor the German governments can rely on. In spite of the euro area’s net surpluses in its fiscal balance and the current account, investors prefer a currency and a country with strong central policy makers which will never default. Investors are also impressed by the tech-heavy structure of the US economy which is an advantage when lots of people work from home, at a time of lockdowns and a steep increase in digital transactions.

- Additional support for the dollar comes from hard-hit emerging and underdeveloped countries whose export revenues have plummeted in the wake of collapsing commodity prices. To service their external debt they have to raise dollars in the open market. There is also anecdotal evidence that a significant part of development aid to these countries is promptly followed by capital exports into foreign accounts denominated in dollars.

COVID 19 will not yet allow of quick turn-around of the world economy

- The main question at this point in time is whether the US economy can indeed be turned around quickly and massively in the second half of 2020. For real GDP to shrink by an average year-on-year rate of 5.9% (as the IMF is predicting), a near-stagnation in the second half of the year is needed, or a stagnation in Q3, followed by a huge expansion in Q4. Since so many people have been losing their jobs since the beginning of the Corona crisis it is unlikely that private consumption, the main component of demand, will rebound quickly enough to make that happen. The public sector may massively increase spending in coming months, but it is hard to imagine that this will compensate for the retreat of private sector demand.

- There are no signs in the US that COVID-19 can be contained in the near-term. Even the usually very optimistic president seems to expect that the number of deaths will rise to 100,000 by the end of the year, from almost 70,000 at this point. It is rather unlikely that this will revive animal spirits over the course of the summer. Profits and stock prices are not about to rebound this year.

European stock markets have suffered most

- As to the euro area’s main index, the EuroStoxx 50 has come down by more than a quarter from its mid-February record high. Investors dislike the large weight of the finance industry, of utilities, car producers, phone companies, and chemicals. The index has the image of representing the old economy and a slow-growth continent. In Q1, real GDP of the euro area declined at an annualized rate of 16.1% (compared to America’s -4.8%). The very high average dividend yield of 4.1% is attractive for investors seeking reliable income rather than growth. On the other hand, the large price decline that has occurred already, together with fairly low price-to-earnings and price-to-book ratios suggest that European stocks might do relatively well in the next sell-out.

- Italy and Spain have been particularly hard hit. They were in the epicenter of Europe’s corona crisis which had brutally laid open the deficiencies of the countries’ health systems. Investors have the impression that Italy will never get out of a recession that is by now 12 years old. Formerly known as a high-inflation country with a structurally weak currency, Italy’s consumer prices will now probably be lower than last year. Spain and Greece are similar in this respect. Dividend yields in the three countries are more than 5% and thus extremely high in real terms.

- I feel that the risk aversion vis-à-vis this group of countries is overdone. Non-Europeans often doubt that the euro area, lacking common fiscal policies and a genuine political union, can survive in the long run. But it is very likely that it will: for the countries in the south, leaving the euro would increase their debt service considerably, extend the recession by several years and cause more unemployment.

- Even populist parties are aware of this and have toned down their anti-euro rhetoric. In the north, a collapse of the Italian, Spanish, Greek and possibly the French economies, combined with large currency depreciations, would also be very expensive. Companies would lose their main export market and be forced to write down the substantial value of the assets they hold in these countries. They have agreed, via the EU Commission and the Council, to launch huge aid packages while the ECB has reduced the standards applied to the quality of the collateral; it is printing money and provides indirect support for the weaker euro countries.

- Letting the euro fail is seen as more expensive than increasing money transfers to the south. In the end, the crisis will lead to some further steps in the direction of European unity. Politicians in the 27 member states are aware that problems like climate change, pandemics and security can no longer be solved by (relatively small) nation states.

bonds do well in today’s deflationary environment

- Government bonds will continue to be a good hedge in mixed portfolios. Their main drivers are expectations about inflation and exchange rates plus the ratings outlook. As the recession might morph into a depression, deflation could once again become a serious risk. No matter how much money is put into circulation, what matters most for wages and consumer, producer or commodity price inflation is the rate of capacity utilization. The lower it is the harder it is to raise prices. Put differently, if potential supply exceeds the demand for products by a large margin, pricing power disappears. Never is there more competition than at times with lots of idle resources. This is the case today. The recent IMF inflation forecasts in the following table are therefore probably too high.

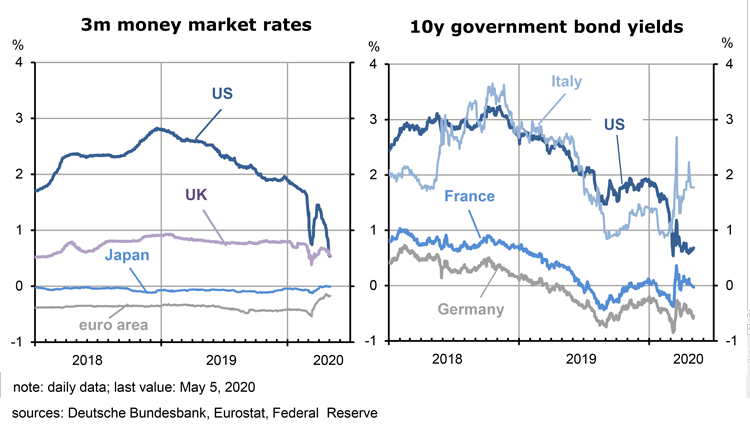

- Investors may wonder why US Treasury yields are presently about 120 basis points higher than German Bunds in the 10-year range. Doesn’t this imply that the dollar will depreciate for ten years by an average of 1.2% against the euro? The dollar is supposed to be today’s safe haven, but then it’s not – because markets seem to bet on its depreciation. On the basis of 10-year breakeven rates, ie, expected average inflation for ten years, the difference is actually smaller: 59 basis points – 1.08% in the US, 0.49% in Germany.

- Since the US output gap will be about eight percentage points larger than in 2019 (the product of 2% trend GDP growth and this year’s growth rate of -5.9%), it is likely that US inflation will be less than the 0.6% average expected by the IMF. In other words, Treasury bond yields will probably continue to decline and move from 0.6% today toward zero or less. The record so far had been in Switzerland: at -1.2%. Since the Fed is close to the lower limit of policy rates by now, the future of US Treasuries depends mostly on incoming inflation and employment data. These continue to point downward. But yields are unlikely to fall below -1.2%. In any case, while real yields of dollar bonds are already in negative territory it is likely that they will fall even further.

- It is tempting to switch to corporate bonds which offer yields well in excess of government bonds. More risk for more yield. But the deep recession that has now begun will be accompanied by a steeply rising number of defaults. Corporate debtors cannot print money. A careful analysis of the financial situation and the prospects of the issuer of the debt is therefore necessary. Sectors that have liquidity problems are airlines, hotels, parts producers in the aircraft industry, small oil firms and retailers, to name just a few.

- Another strategy for fixed income investors is to bet on the widening or narrowing of yield differentials. The spread in the 10-year maturity between Greek, Italian and Spanish government bonds and German Bunds is 268, 242 and 133 basis points, respectively. If you trust me that the euro will not blow up any time soon, it pays to short Bunds and go long the three other bond markets. This way it is also possible to eliminate exchange rate risks.

- One thing is a near-certainty: monetary policies will remain very expansionary. Central banks attempt to develop new tools in order to provide even more stimulus. This suggests, as a general rule in the present environment, to borrow at the short end of the yield curve and invest at the longer end. This is a bet on the ongoing flattening (possibly the inversion) of the yield curve.

oil producers are in trouble as oil prices have tumbled

- Import prices are an important determinant of general inflation in a country. For decades, the oil price played a major role in this regard. Following the rapid expansion of ever cheaper alternative energy from wind and solar, oil is getting less important over time, but remains very important because it is the largest single component of the import bill of most European countries, as well as those of China, Japan and South Korea. Oil production and demand had increased steadily year after year at rates of 1 to 1 ½% per year, to almost 100 million barrels a day. Burning oil and other fossil fuels such as coal and gas has been the main culprit for the dangerous increase of the world’s temperature.

- Because the Corona virus has forced governments across the world to restrict mobility in order to reduce infections, air and road traffic has declined dramatically. Large parts of the population do not move around much anymore, long-distance tourism and business travel have de facto been suspended. Cruise ships, buses and airplanes, but also football games, marathons, concerts, trade fairs and non-digital conferences are regarded as dangerous traps where it is not possible to avoid getting infected by the virus. Lots of events have been called off.

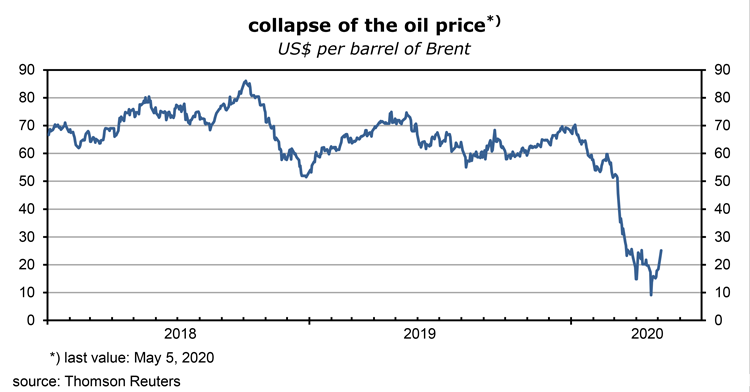

- At this point, the demand for crude seems to be roughly one third lower than one year ago while the oil cartel has cut output by about ten percent. The result is a huge disequilibrium between demand and supply. It has been so extreme that oil storage tanks are flowing over. On the last trading of the May futures contract, the oil price fell to almost minus 40 dollars. In Europe, the spot price of a barrel of North Sea oil had been $25 today, compared to about 70 dollars at the turn of the year. It will remain low for the foreseeable future.

- For oil importing countries this has boosted real disposable income and has thus stabilized overall demand and employment, if only at the margin. For oil producers and exporters, usually poor countries, this has been a catastrophe. It is a zero-sum game, after all. Government budgets in these countries are often based on a certain, much higher oil price and can now no longer be balanced. Once currency reserves have been depleted, debt markets have to be tapped which in turn raises the interest rates these debtors must pay. Austerity and a reduction of living standards follow, and probably social unrest and regime change as well, if oil prices stay low for an extended period (which would be my assumption today). Russia, Brazil, Nigeria and even Saudi Arabia come to mind. Corona will have major geopolitical effects.

some other conclusions

- Here is a non-systematic and non-comprehensive list of the changes that the Corona crisis will bring about. Investors must take into account these developments – they have significant strategic implications:

- “reshoring” will be an issue as firms cannot rely on uninterrupted supply chains any more; globalization takes a break

- monetized fiscal deficits (money printing) will not lead to higher inflation if output gaps remain large; Japan has shown that it can work

- there will be a massive increase in spending on health care and epidemiological research

- to maintain open borders, European governments have to streamline their health systems

- deflation is back on the radar screen

- China catches up with the US, not only in terms of purchasing power parities but also in terms of market exchange rates (GDP growth rates continue to differ strongly)

- economic stimulus programs will come with more environmental requirements than in the past

- the neo-liberal business model leads to unfair outcomes and will gradually be phased out in favor of more government intervention in markets

- monetary policies are of little use in a deep crisis once the lower zero bound for interest rates has been reached

- fiscal policies will be the most effective tools for years to come

- European-style shock absorbers will be introduced in countries where unemployment has reached dangerous dimensions

- … to be filled in by the reader …

Read the full article in PDF format:

Wermuths Investment Outlook May 5, 2020